* FCF (Free Cash Flow) : 올해 영업활동으로 번돈에서 올해 투자한 돈 빼고 남은 돈 (삼성전자 : 영업활동 70조 벌고, 30조 투자해서 40조(FCF)에 대한 50%인 20조를 배당으로 줌)

* RE : 배당 다 주고 남은 돈

Los 17.a) Objective of financial reporting and the importance of financial reporting standards in security analysis and valuation.

재무보고서(Financial Reporting)의 목적 : 현재 및 잠재적 투자자, 채권자들에게 기업에 대한 의사결정에 유용한 정보 제공 (The objective of financial reporting is to provide information about the firm to current and potential investors and creditors that is useful for making their decisions about investing in or lending to the firm)

보고기준(Reporting Standards)은 기업들이 거래들에 대해 비슷하게 보고할 수 있게 하지만 경영진들의 융통성 및 재량권도 남아있어야 한다.

★재무보고는 Valuation(기업가치)를 위해 설계된 것이 아님을 알아야 한다. - 기업가치 산정을 위한 중요한 요소를 제공하긴 하지만 재무제표상의 Net Asset이 기업 시가총액과 동일하지 않은 이유가 바로 재무제표 숫자가 기업가치를 나타나는게 아님을 의미한다 - 바로 재무보고가 여러가지 가치(공정가치, 원가, 내재가치 등)가 혼재되어 있기 때문이고, 모든 가치(인적가치, 브랜드 가치 등)를 포함하지 않기 때문이다.)

Los 17.b) The roles of financial reporting standard-setting bodies and regulatory authorities.

Standard-setting bodies(표준화기구) - 재무회계기준을 설립하는 회계사, 감사인들로 이루어진 전문기관 ⓐ FASB (Financial Accounting Standards Board) - 미국 재무회계기준위원회 → GAAP제정 ⓑ IASB (International Accounting Standards Board) - 국제회계기준 위원회 → IFRS 제정

Regulatory Authorities(규제기관) - 재무보고 기준을 준수할 수 있도록 법적으로 강제하는 기관 ⓐ SEC (Securities and Exchange Commission) - 증권관리위원회 (FASB가 제정한 회계기준을 SEC가 인정해줌) - SEC의 요구사항에 따라 미국기업들은 재무보고를 해야함.

IPO시 제출해야하는 보고서 - IPO 개괄 (the Offering) - 감사 재무보고서, 위험평가, 인수기관 등

Form 10-K

사업보고서 (연간 보고서, 연1회) - 회계감사(Audited)된 자료

Form 10-Q

분기보고서 (회계감사되어있진 않음) *미국이 아닌 기업은 6-K로 반기보고서 제출

Form DEF-14A

Proxy Statement - 기업 경영진에 대한 보상 및 의결권있는 주주들에 대한 회사 주요사항등에 대한 정보 - 경영진 보수 및 스톡옵션 확인 가능함 - 기업의 지배구조, 이사회, 주총 선출후보 프로필, 주주총회 안건 등 확인 가능 (헤지펀드에서 반드시 확인하는 공시)

Form 8-K

중요한 이벤트나 중요한 자산 인수, 처분, 경영진의 변동, 기업 거버넌스 등 회계관련 문제 등이 있을 때 공시 8-K공시가 요구하는 기업상황 : 파산/구조조정/M&A/유상증자/부채 등 새로운 자금조달/경영진 교체나 이사회 구성변화 등등

Form 144

SEC에 등록하지 않고 증권을 발행할 수 있지만 '증권을 발행할 의사'를 반드시 SEC에 공시해야 함.

Forms 3,4,5

내부자 주식거래내역 (기업 임원 및 이사회 등의 지분거래내역) - Form 3 : 내부자(Insiders)가 처음 지분 획득 시 공개 자료 - Form4 : 이후 주식보유현황 변동내역 공개 자료 - Form5 : 내부자의 지분거래내역에 대한 연간 보고서

DEFM-1A, S-4

M&A 관련 공시보고서 - S-4가 더 자세하게 인수에 관련된 모든 내용을 담은 보고서 (인수합병 개요, 타당성, 딜 성사 조건 및 일정 등)

FORM 10-12B

기업 분할과 관련된 공시보고서

* DEFM-14A 란? - Definitive proxy statement relating to a merger, acquisition, or disposition Merger Proxy * DEF란? - defintive proxy

IPS (Invesetment Policy Statement) → 고객에 대한 이해 자료 → Risk, Return, Others * communication instrument allowing clients and portfolio managers to mutually establish investment objectives and constraints.

<Components>

Return Objective

Risk Objective

Constraints (Liquidity, Regulations 등)

Evaluation

<Risk & Return Objective>

Absoulute : 수치 언급 (비교대상 없음)

Relative BM 언급 (ex: LIBOR)

Los 64.d) Willingness & Ability ★

- Ability to take risk : 재무상태에서 기반 (투자기간 및 자산규모에 비례) - Willingness to take risk : Attitude에서 기반

Willingness

Ability

높음

낮음

높음

적절

이유를 찾아 Educate

낮음

낮은 Risk선택 유도(주제파악하렴)

적절

Los 64.e) Constraints

- Liquidity : 바로 현금으로 전환이 필요한 때 고려 (ex. 손해보험사) - Time-Horizon : 투자기간 고려, Longer Time은 More Risk taking가능 - Tax Situation : 개인 투자자들에게 특히 중요 * Tax Deferred Accounts : 출구 과세 (나중에 세금) * Tax Exempt Accouts : 입구 과세 (처음에 세금) - Legal & Regulatory : 금융기관, 기관마다 적용되는 법을 고려 - Unique Circumstance : 투자자별로 가지고 있는 특징들 고려

Los 64.f,g) Asset allocation & Role

- After IPS → Strategic Asset Allocation 결정 (자산별 비중, Risk, Return, Correlation고려) - 과거에는 주식, 채권, 부동산 고려 → AI의 발달로 종목 증가 - Role) 고객의 Return & Risk를 위해 자산 분배

* Deviation 발생 → Short term 이익을 위해 잠시 Active 하게 운영 = Tactical Asset Allocation(전술적 자산배분) * Strategic Asset allocation(전략적자산배분- 모범답안) & Tactical Asset Allocation(전술적 자산배분, 시장에서의 Chance에 따라 모범답안에서 조금 바뀔 수 있는 전략) * Tatical Asset allocation is the decision to deliberately deviate from the policy portfolio (deviate from the strategic asset allocation)

- Core-Satellite Approach: Passive(major) + 다수의 Active(minor) * Core-satellite investing is a method of portfolio construction designed to minimize costs, tax liability, and volatility while providing an opportunity to outperform the broad stock market as a whole. The core of the portfolio consists of passive investments that track major market indices, such as the Standard and Poor's 500 Index (S&P 500). Additional positions, known as satellites, are added to the portfolio in the form of actively managed investments. (핵심 Core는 Passive + 위성은 Active집중투자)

Los 64.h) ESG Trend

- Environmental, Social, Governance(ESG)를 잘하는 기업에 투자하는 Trend ⓐ Negative Screening : 여긴 투자 x (ex. 담배회사, 석탄회사 등) ⓑ Positive Screening : 여긴 투자하자 (ex. 사회적기여기업)

- Enganement / Active owenership investing : 주주로써 권한을 행사 (주주총회 참석)

Los 65.a,b) Cognitive errors vs Emotional biases & 종류

- Cognitive errors(인지오류) : 합리성 부족이 원인, 그나마 고칠 수 있음. - Emotional biases(감정편향) : 감정이 원인, 고치기 어려움 * 각각 독립적으로 나타나기도 하고, 둘다 나타나기도 한다.

Cognitive errors (인지 오류)

Belief Perseverance(믿음에서 비롯되는 오류)

1. Conservatism bias

초기 판단 고수, 새로운 정보에도 의견을 바꾸지 않음. (P/F가 시장변화에 대응X)

2. Confirmation bias

확증편향, 자기 의견에 맞는 정보만 찾으려고 함.

3. Representativeness bias

대표성 편향, 기존 이미지로 대충 판단 - Base-rate neglect : 기저율 무시, 이미지로만 판단 - Sample size neglect : small sample이 전체 대변 오류

4. Illusion of control bias

자신이 결과를 통제할 수 있을 거라는 믿음 → Emotional bias의 illusion of knowledge, self-attribution, overconfidence와 연관

5. Hindsight bias

사후 과잉 확신 편향 "내가 그럴 줄 알았어."

Information processing bias (정보처리에서 비롯되는 오류)

1. Anchoring & Adjustment bias

새로운 정보가 와도 기존 결론에 더 가중치를 둠

2. Mental Accounting bias

Overall P/F 관점으로 생각하지 않음. 돈에 꼬리표를 붙임

3. Framing bias

의사결정이 Frame에 영향 (어떻게 보여주냐에 따라 결과가 다른 것)

4. Availability bias

쉽게 기억하는 정보에 더 집중함 (최근거, 직접 경험한 것)

Emotional bias

1. Loss-Aversion bias

같은 금액이어도 이득보다 손해에 더 고통

2. Overconfidence bias

근자감 (Illusion of knowledge, Self-attribution bias, Self-enhancing, Self-protectig, Prediction overconfidence)

3. Self-control bias

나중에 어떻게든 되겠지(YOLO) hyperbolic discounting(미래 효익을 평가절하)

4.Status quo bias

변화를 싫어함

5. Endowment bias

기존자산에 대한 애착

6. Regret aversion bias - Errors of commision(했는데 나중에 틀린거 후회 큰비중) - Errors of omission (안했는데 틀린판단인거 후회 낮은 비중) - Herding behavior (나중에 후회할까봐 남들하는대로)

아무것도 안하는 것 (했다가 후회하며 어쩌지?)

Los 65.c) Behavioral bias & Market

- 행동경제학은 기존의 경제학이 설명해주지 못한 시장의 이상현상에 대해 설명이 가능함

- Overconfidence : Overtrading, Risk평가절하, 낮은 분산화

- Self-attribution bias : overconfidence & hindsight bias초래 - Confirmation bias : 새로운 정보 무시 - Anchoring : 최근 고점이 적절한 가격이라고 믿음 (가격을 떡락 중인데) - Fear of regret : very skeptical investor양산 - Halo effect (후광효과) : 주가가 오른 회사의 제품은 다 이뻐보이는 것 - Home Bias : 익숙한 국가에만 투자하는 경향

1. Holding Period Return (HPR) : Simply the % of increase (시간고려 X) - (기말 value / 기초 value ) -1

2. Average Return ⓐ Arithmetic mean (산술평균) : [R1+R2+....+Rn]/n ⓑ Geometric mean (기하평균) : Compounded Annual Return(연평균복리수익률)

3. Other Return - Gross Return : Fee 차감 전 & Net return : Fee 차감 후 (둘다 거래 비용은 차감함) - Pretax nominal return : 세전 & After tax nominal return : 세후 - Real return : Inflation차감, 구매력 반영 - Leveraged return : 파생상품 return *Margin & Debt고려

62.b) Money weighted Return vs. Time Weighted Return

1. Money weighted Return (IRR개념) - CF Timing 및 CF규모에 영향을 받아서 조작가능성이 존재함 - 계산기 사용법 숙지 필요 (돈을 투자하는 것은 -, 돈이 들어오는 것은 + 부호 사용 주의)

2. Time weighted Return (Compound growth개념) - 각 구간별 HPR들을 곱한 후 평균 수익률을 측정함 - √(1+HPR1)*(1+HPR2) -1 - CF timing 및 규모에 영향을 받지 않음 → 성과평가에 더 적절한 지표

62.c) Characteristics - 투자 시 → Trade off Between Risk & Return + Liquidity도 고려 필요 - Small cap : 수익률 높음, Risk 높음 & T-bill : 수익률 낮음, Risk 낮음 - Return : Negative Skewed, Greater Kurtosis (Fat-Tail) → 오른쪽으로 더 두꺼운 꼬리, 첨도가 높음 → Large downside, Frequent Extreame Results

62.d) Risk aversion - Risk Averse : 위험 회피 성향 (같은 수익률이면 낮은 위험 선택) * EI에 나오는 Loss Aversion은 수익을 얻는 것보다도 손실을 더 싫어한다는 것 (행동경제학) - Risk Seeking : 위험 선호 - Risk Neutral : 위험 중립, 위험에 대한 관심 자체가 없는 것. - Risk Averse : 투자자라도 수익률이 높으면 Risky Asset 선택 가능 (Compensation)

62.e) Selection - Utility function : 효용함수 (Risk & Return관련)

- Indifference curve : 무차별곡선 (Risk & Return조합 구성), 그래프 위의 지점은 모두 같은 효용 - Risk Averse 투자자 -> 위험 증가에 따라 더 많은 수익 필요 (Adverse할수록 그래프가 더 Steep해진다)

62.i) Efficient Frontier - 자산 비중에 따라 각각 최소 위험의 P/F = Minimum Variance P/F ▷ 최소분산선 (Minimum variance frontier) : 주어진 기대수익률 하에서 분산(위험)이 가장 작은 포트폴리오의 집합 (주어진 기대수익률(E(r))하에서 가장 표준편차가 낮은 포트폴리오)

▷ 효율적 프론티어 (Markowitz Efficient fontier) : 최소분산 프론티어 중에서 주어진 위험 하에서 가장 수익률이 높은 포트폴리오의 집합 ▷ 최소분산포트폴리오 (GMVP; Global Minimum variance portfolio) : 효율적 프론티어 상에서 가장 위험이 낮은 포트폴리오

- Risk Averse 투자자 : 최소위험 & 최대이익 P/F 선택 (=Efficient Frontier 위에서 선택)

- The greatest expected rutrn for each level of risk => Efficient Frontier - Efficient Frontier + 무차별 곡선 => 각 개인들의 최적의 P/F

* Optimal risky portfolio - 효율적 프론티어 위의점 * Optimal investor portfolico - CAL과 무차별곡선이 접하는 점

문) The set of portfolio on the minimum-variance frontier that dominates all sets of portfolios below the global-minimum-variance potfolio is the : A. capital allication line. B. Markowitz efficient frontier.

C. set of optimal risky portfolios

정답) B 최소분산경계선 중에 우세한 선들 포트폴리오 => 효율적 프런티어

63(모두가 다른선호를 가지고 있다는 것을 제거, 공통된선 추출).a,b) Implication, CML

1. With Risk Free assets → Sigma_p = W_A * Simga_A → CAL (Capital Allocation Line도출) - CAL과 무차별곡선이 접하는 곳에서 개인의 P/F가 결정됨 (개인의 위험회피 정도마다 선택이 다 다름) 2. 그래서 Modern P/F가정 : Homogeneous Expectation → Same P/F (Same efficient frontier) → Market P/F → Capital Market Line도출 : 기대수익률(E) = Rf + Risk Premium (CAL의 특별한 case가 CML로 Optimal risky portfolio가 Market Portfolio가 된다)

CAL Capital Asset Line

CML Capital Market Line

RF + Risk Asset

RF + Modern P/F

개인 무차별곡선마다 P/F다름

모두가 같은 P/F선택

63.c) Systematic risk

1. P/F Risk → Less than (개별주식의 Risk의 총합) - 감소될 수 있는 위험 : Unsystematic Risk (비체계적 위험) = unique, diversifiable, firm-specific risk - 감소될 수 없는 위험 : Systematic Risk (체계적 위험) = nondiversifiable risk = market risk

2. Total Risk = Systematic + Unsystematic - N (포트폴리오 안의 주식 수)가 증가할 수록 Unsystematic은 감소 - Unsystematic 위험은 Manager 재량으로 감소가 가능 → Return Reward는 오직 Systematic으로부터 온다 (결론) Only systematic risk is priced. Investors do not receive any return for accepting nonsystematic or diversifiable risk.

63.d, e) Return Generating Model, Beta 1. 기대수익률 = RF + beta1*F1 + beta2*F2 +... Beta = 민감도, 1개면 Single Model, 2개 이상이면 Multi-factor Model

2. Multifactor Model - Macroeconomic ex) GDP, Inflation, Export - Fundamental ex) Earnings, Size, 매출액 등 - Statistical (잘안씀) ex) Data mining

3. Market Model : Ri = @ + Beta*Rm + e (Beta에 따라 수익률이 변화) -> Security Characteristic line

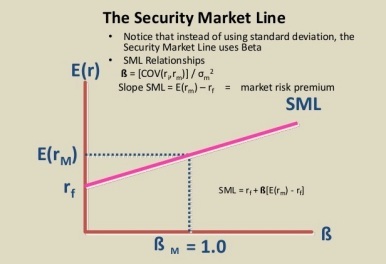

4. β (Beta) - 시장변화 % 대비 움직이는 민감도 βi = [covariance of Asset i's return with the market return] / [variance of the market return]

시장변화 % = Systematic Risk = Market Risk = β

(The average beta of all assets in the market = 1)

Los61.a) P/F Approach - P/F Perspective = 포트폴리오 안의 개별주식의 Risk, Return의 총합 (The portfolio perspective refers to evaluating individual investments by their contribution to the risk and return of an investor's portfolio) → Reduce risk without reducing return (diversification allows an investor to reduce portfolio risk without necessarily reducing the portfolio's expected return) - 1950, Harry Markowitz → 상관관계가 1보다 작다면 Reducing Risk가능 주장 (상관관계가 1이면 분산효과x) (Unless the returns of the risky assets are perfectly positvely correlated, risk is reduced by diversifying across assets.) <Modern Portfolio Theory (MPT)> - Diversification Ratio = (P/F안에서의 %) / (개별로 있을떄 %) → Risk 감소 - 낮을수록 분산으로 인한 리스크경감효과가 크다는 것을 의미 * 분산효과는 시장이 정상일 때 가능 (공포앞에서는 상관관계 소용x, 같이 움직인다 - market turmoil, credit contagion)

Los61.b) PM Process 1. Planning : Analysis, IPS 작성 - 투자자의 위험용인정도, 수익률 목표, 투자기간, 세금문제, 유동성문제, 소득 등 투자자 선호 파악 - 파악해서 IPS(Investment policy statement ; 투자계획서)를 작성 (투자목표, 벤치마크 투자목표(매니저 성과평가지표) 기술) - IPS는 주기적으로 투자자의 목표나 제약상황이 유의미하게 변했을 때마다 업데이트 (수시로x) 2. Execution : Asset type 결정(asset allocation), Top-down approach, Bottom-up approach 3. Feedback : 상황변화 체크, IPS Update - IPS는 상황, 시간이 변해야 업데이트 함. (주기적으로는 ok, but 너무 자주는 말고) - 경제상황 등 투자조건이 변하는지 모니터링 및 rebalancing 진행

Los61.c) Investor 타입, 특징 ★ 시험에 잘나옴!

Investor type

Risk Tolerance

Investment Horizon

Liquidity Needs

Income Needs

Individual

Depends on Indivdual

Depends on Indivdual

Depends on Indivdual

Depends on Indivdual

Endowment&Foundation

High

★Long - 보통 가장 김(perpetual lives)

Low

Spending level

Bank

Low

Short

Adequate or High

Pay interest

Insurance

Low

Life(생보) - Long P&C(손보) - Short

High

Low

DB pension

High

Long

Low

Depens on age

Mutual Fund

Depends on Fund

Depends on Fund

High

Depends on Fund

- Mutual Fund : Style마다 운용방식이 다름 - Soverign Fund : 국부펀드 (나라에서 운영)

Los61.d) DC & DB

DC : " Defined Contribution" - 정해진 납입금, 위험은 납입자가! (The firm makes no promise to the employee regarding the future value of the plan assets. The investment decisions are left to the employee, who assumes all of the investment risk)

DB : " Defined Benefit" - 정해진 수익, 위험은 회사가! (The firm promises to make periodic payments to employees after retirement The employee's future benefit is defined, the employer assumes the investment risk)

Los61.e) Asset management Industry

Client → $ → Fund 운용 (Buyside) ← Broker, IB(Sell Side)

운용방식 : Active(∂가 목표) vs Passive - Active : BM Outperform목표, High Fee - Passive : Index 추종, Smart Beta(Beta보다 살짝 더 높은 수익률 추구하는 것), Low fee

최근 트렌드 : Passive 증가, Data 증가, Robo advisors 등장 * Passive management의 시장점유율은 올라가고 있음. (낮은 fee, 선진 시장의 Active managing에 대한 의문)

Los61.f) Investment Product

Mutual fund : 돈을 모아서 하나의 투자단위를 결성 → pooled investment → Net Asset Value(NAV)로 측정 ① open-end fund (개방형펀드): 언제든 NAV로 추가투자 or 환매 가능 - 개방형 펀드는 펀드의 지분 수가 고정되어 있지 않은 것으로 펀드는 일반투자자의 수요에 따라 새로이 지분을 발행할 수 있으며 투자자는 지분을 순자산 가치로 매각할 수 있다. - Load fund : 로드 펀드 - 수수료 O (판매 수수료를 포함시킨 가격으로 판매되는 투자 신탁) - No Load fund : 수수료 X (브로커나 세일즈맨을 거치지 않고 판매되는 뮤추얼 펀드로, 판매수수료를 징수하지 않는다) ② Close-end fund (페쇠형펀드) : Fund Size 고정, 추가투자 못함 → 펀드의 지분은 주식처럼 거래됨 (Trade like equity) → NAV로 거래 안될 가능성이 높다. * Mutual Fund가 ETF보다 수수료 높은편, 대신 Brokerage cost는 없음.

Money market fund : Invetment in Short term debt, low risk

Bond mutual fund : Investment in fixed-income

Stock mutual fund : Investment in equity - Passively managed (ex. Index fund) - Actively managed (Manager가 직접운용, High turn over, Tax 많이, 자주냄) - ETF(Exchange Traded Funds) : Close-end 같이 수량이 정해지고, 특성 Index를 추종. 장에서 거래되기 때문에 NAV에 밀접하게 거래된다. Tax에 유리 - Seperately Managed Accounts : Single-Investor를 위한 계정 (돈많은 분들)

Q1. With respect to formation of portfolios, which of the following statements is most accurate? A. Portfolio affects risk less than returns. B. Portfolio affects risk more than returns. C. Portfolio affects risk and returns equally.

정답) B *포트폴리오분산화효과로 risk reduction이 된다는것은 Return보다 risk에 더 큰 영향을 준다는 것!

Q2. A defined benefit plan with a large number of retirees is likely to have a high need for : A. Income B. Liquidity C. Insuarance

정답) A *DB연금은 유동성보다도 Income cash flow가 더 중요함!

Q3. Which of the following financial products is least likely to have a capital gain distribution? A. Exchange traded funds B. Open-end mutual funds C. Closed-end mutual funds

정답) A (ETF는 지수추종이기때문에 capital gain 배당은 없음. 물론 가격변동에 의해서 capital gain sale은 가능하지만, capital gain distribution과는 구분필요!)

Q4. Which of the following pooled investments is most likely characterized by a few large investments? A. Hedge funds B. Buyout funds C. Venture capital funds. 정답)B - Hedge fund : 전략이 다양함.. - Buyout funds : 비상장회사에 대해 적은 수의 투자가 이루어짐 - VC funds : Short time horizon, many small investments (수가 많음) 그러므로C는 x

Los66.a) Risk Management - Process : Identify risk tolerance → Measure the risk → Monitor & Modify risk - Risk Management는 Risk를 제거하는 것이 아님, 피하는 것도 아님. - Risk free rate보다 더 벌려면 → Risk Taking이 필요 **그래도 Return이 가장 1순위다(Return높은거? Risk낮은거? => Return높은거가 우선!) ① 정해진 Risk수준에서 Return 극대화 (ㅇ) ② 정해진 Return에서 Risk 최소화 (X)

※ Risk Vs Danger : Risk는 "불확실성(uncertainty)"을 의미 => Risk가 나쁜가? 무조건 나쁜 것이 아니라 수익률을 높이기 위해서는 적절한 taking이 필요한 것. * Return을 높이려면 → Risk taking high가 필요 그러나 High risk taking을 한다고 해서 High return이 보장되는 것은 아님 => Risk Management의 목표는 Risk의 제거가 아님. 제거가 아니라 목표달성을 위한 적절한 Risk Taking이 목표임! ** Position Limit이 아님 (위험관리가 투자를 제한하는 것을 의미x)

Los66.b) Frame work - Establishing process (risk governance) - Risk tolerance결정 - Measuring Risk - Managing, Mitigating Risk - Monitoring Risk - Communication - Analysis → Goal 과 Risk의 "Align"

Los66.c, d,e) Risk Governance & Risk Tolerance & Risk Budgeting - Risk governance : 운용의 목적에 맞게 Risk Tolerance를 결정 (From Top Management(윗선 관리자가 결정)) → Managing Risk (Risk governance refers to senior management's determination of the risk tolerance of the organization, the elements of its optimal risk exposure strategy, and the framework for oversight of the risk management function.) - Risk Tolerance : 목적 달성을 위해 Risk를 Taking할 수 있는 정도 (Inside와 Outside 위험 모두 고려) - Risk Budgeting : 위험을 고려하여 Allocating firm resource to assets (Risk budgeting is the process ofallocating firm resources to assets (or investments by considering their various risk characteristics and how they combine to meet the organization's risk tolerance.) ① 기준에 따라 허용가능한 위험의 정량화 (quantifying tolerable risk by specific metircs) ② 투자 리스크 특성에 따른 자산 배분 (allocating a portfolio by some risk characteristics of the investments)

→ Risk들이 서로 Mix 되어, 최적의 수익률이 나올 수 있도록 함 (ex. Beta로 분배, Duration을 정하는 등) * Position Limit(행동제한)은 Risk Budgeting이 아님 주의

Los66.f) Risk type

★Financial Risk

Credit Risk

디폴트 나고 배째고 안갚음

Liquidity Risk

제값에 안팔림

Market Risk

가격폭락

Non Financial Risk

Operation Risk

운영상의 Error

Solvency Risk

파산

Regulatory Risk

규정변화

Political Risk

정부, Tax

Legal Risk

고소, 소송

Model Risk

잘못된 계산

Tail Risk

블랙스완, 극단적인 결과값

Accounting Risk

회계정책의 변화

개인의 Risk

Mortality Risk

사망위험(Life Insuarnce로 대비 - 생명보험)

Longevity Risk

장수위험 (Life time Annuity - 연금으로 대비)

* Risk들은 독립적이지 않음 → 같이 상호 영향 (영향을 고려해야)

Los66.g) Method - Standard deviation : Volatility 측정, Non-normal 에서는 활용 불가 - Beta : Equity Risk측정 - Duration : 이자율 변화에 대한 채권의 민감도

- Derivative Risk - Delta : Underlying asset의 변화 - Gamma : Delta변화율의 변화

- Vega : 변동성의 변화 - Rho : Risk free rate의 변화에 대한 파생상품 가치의 민감도 Value at Risk(VaR) : 특정확률 안에서의 minimum loss (Value ar risk is the minimum loss over a period that will occur with a specific porbability.) Conditional VaR(CVaR) : 최소 손실을 넘어서는 손실액 측정

- Subjective Estimates ① Stress testing : 특정 변수의 극단값 테스트 ② Scenario Analysis : 변수들의 변화 테스트 ③ 극단적 사건 예측은 어려움 -> Data 근거가 x -> 차라리 Subjective estimate이 도움이 될 수 있음. (차라리 주관적으로 상상해서 예측하는게 더 나을 수 있다) * Risk자체를 없앨 수는 없음 → 결국 Diversification이 답! & Risk 관리는 항상 Cost & benefit고려가 필요함

Self Insuarance (bear a risk)

적립금 계정

ex. 충당금

Risk Transfer

위험 전이

ex. 보험, Benefit & Costs는 항상 고민해야 (보험료 얼마 보험금 얼마 등) - Surety bond (보증증서) - Fidelity bond(신원보증보험)

Risk Shifting

위험 방향 바꾸기

ex. 파생상품 (Put, Call)

Q5. Which of the following best describes activities that are supported by a risk management infrastructure? A. Risk tolerance, budgeting, and reporting

B. Risk tolerance, measurement, and monitoring C. Risk identification, measurement, and monitoring 정답) C - 리스크 인식 -> 측정 -> 모니터링이 risk management process라는거 기억하기!

Q6. Effective risk governance in an enterprise provides guidance on all of the follwing except : A. Unacceptable risks.

B. worst losses that may be tolerated. C. Specific methods to mitigate risk for each subsidary in the enterprise. 정답) C - Risk governance는 위험경감을 위한 구체적인 방법을 지정하는 것이 아니라 오히려 위험용인 정도를 설정하는 것이므로 정답이 아님.

Q7. A firm's risk management committee would be expected to do all of the following except: A. Approving the governing body's proposed risk policies.

B. deliberating the governing body's risk policies at the operational level. C. providing top decision-makers with a forum for considering risk management issues. 정답) A - A (제안된 위험정책의 승인), B(운영수준의 리스정책 심의), C(최고의사결정자에게 리스크 이슈 전달) - 리스크관리 위원회는 운영수준에서 리스크 관리를 고려하지 위험정책을 결정짓고 승인하는 단계는 X(리스크위원회는 운영단계)

Early Stage에 투자 -> Venture Capital Fee : 투자할 때 & Fund를 결성할 때 & 투자 회수할 때 각각 LP와 협상해서 조율

<Private Equity Strategies> ① Leveraged buyouts(LBOs) : Fund를 Debt으로 Financing 해서 조성 > Debt : Bank Debt or High-yield bonds or Mezzanine * Mezzanine : 보통 후순위채보다 아래로 주식가치 증가할 때 주식으로 전환 가능 - PE는 기업 인수 후, 추후 재매각을 위하여 Firm의 value 상승을 도모

- High Cash flow firm : 조달한 Debt을 상환할 수 있기에 LBO에 매력적

- LBO Type : Management buyouts (MBO, 기존 경영진이 회사 인수), Management Buy-ins (MBIs, 외부 경영진이 회사 인수) - Developmental capital or Minority equity investing : 소수지분 투자로 회사 Value-up에 도움 (Private investment in public equities (PIPEs) - 공공주식에 대한 민간투자)

② Venture capital : early stage, high risk, but high return

회사의 가치 상승을 위하여 경영에 직접 관여

The entire PE continuum

Ventural capital

start-up & seed-satge businesses

Growth equity

more established businesses

Buyouts/LBOs

mature businesses

<VC는 Stage에 따라 분류 (순서 시험에 잘나옴!!)> 1. Formative stage : 이제 막 회사가 형성되기 시작하는 단계 ① Angel investing or pre-seed capital : "Idea" 단계 (주로 개인이 투자)

② Seed Stage or Seed capital : "Product(시제품) 생산" 단계 (VC가 투자 시작) * initial investment단계, the first stage of financing. ③ Early Stage or Start-up Phase : "상업화" 단계, VC 추가 투자 가능

2. Later Stage (=expansion venture capital) : 상업화 운영 단계, 추가 "확장"을 위해 funding 3. Mezzanine-Stage : "IPO" 준비 단계, Funding 타이밍 중요

1. Trade Sale : 보유 지분을 다른 회사에게 매각 (VC → SI) 2. IPO : 상장 시킨 후 매각

3. Recapitalization (Re-cap, 자본재조정) : 대출 받아서 배당금으로 사용, 엄밀하게 Exit은 아님 4. Secondary Sale : 다른 PE에게 지분 매각 (VC → VC) 5. Write-off / Liquidation : 투자 실패의 경우 청산

<PE의 Benefit & Risk> - PE의 평균수익률은 주식보다 높은 편, TI와의 상관관계도 1보다 낮기 때문에 P/F포함 시 분산효과 有 - PE의 평균 표준편차는 TI보다 높음 (더 위험한 투자상품 *그러나 mark to market이 많지 않아 변동성이 적게 보일 수 있음) - PE도 Hedge fund와 마찬가지로 survivorship & Back-fill bias 존재 -> Return up ward (수익좋은것만 살아남아서 좋아보이는 것 처럼 보이는 편향 존재) - PE는 비상장이므로 Revalued infrequently -> 상관계수 측정할 때 downward bias존재 - PE는 Leverage를 많이 씀 -> 이자율 영향과 가용자금 상태 체크 필요 - 투자 전에 PE의 Manager, Valuation Method, Fee구조 등 면밀히 체크해야 함.

Los 60.b) Private Debt

1. Direct Lending : 직접 대출, 주관사 없음 (Leverage를 일으켜서 돈을 빌려주기도 함 *leveraged loan) 2. Venture Debt : Start-up Phase 회사에 대출 (*CB/BW형태 多) 3. Mezzanine Loans : 후순위 부채로 투자 (CB, BW 등) 4. Distressed Debt : 재무적으로 어려운 성숙된 기업의 부채를 매입, 경영권에 관여, 회사 구조조정 -> 회사 부활 -> 채권 가격 상승 (Vulture investor)

<Risk & Return> - 어느 곳에 돈을 대출해주냐에 따라 Risk는 천차만별 + illiquidity 존재 -> 때문에 일반 상장사들의 채권에 투자하는 것보다는 수익률이 좋음. - PE, VC, Private Debt 모두 Value-add를 위하여 경영에 관여

Los 60.c) Real Estate

- Real Estate에 투자 : 임대료 + Capital gain + P/F분산효과 + Inflation Hedge가능 - 투자방식 : 주거용 부동산, 상업용 부동산, 부동산의 대출금(모기지)에 투자 (*주거용 부동산이 상업용보다 규모나 가치가 훨씬 큼 유의)

Residential Property : 보통 대출(모기지)와 함께 주거용 부동산 구매 → 대출자(lender)는 모기지들을 모아서 pool을 만들고 그 pool에 대한 증권발행 → MBS - MBS 구매자들은 개별자산들에게 간접적으로 투자한 효과 (부동산 가격이 변동하면 대출자의 Equity가 변동)

Commercial real estate : 임대료(rent)가 주요 수익 - Long-time horizons, illiquidity, 큰 투자규모 등으로 인해서 많은 투자자들에게 상업부동산에 대한 직접 투자는 적합하지 않음. → 대안1. 부동산에 투자하는 Limited Partnership의 지분 구매 & 대안2. REIT 구매

* 직접 특정 모기지에 투자 → Direct Investment * MBS를 구매 → Indirect Investment * REITs : 부동산에 투자하는 Fund의 지분을 발행해서 장내에 주식처럼 거래하게 만든 상품 - Tax Benefit을 위해서는 투자소득의 90%이상이 배당으로 쓰여야 함. - 투자자는 REITs에 투자함으로써 간접적으로 부동산에 투자하는 효과를 누림.

Benefit & Risk ① Real Estate의 성과 측정 ⓐ NCREIF(감정평가; National Counil of Real Estate Investement Fiduciaries) : Appraisal Index, Real Time이 아니기 때문에 Smoothing경향, 낮은 표준편차 ⓑ Repeat Sales : 특정 부동산이 거래되는 가격을 반영 (Sample Selection bias존재, 전체반영 불가) ⓒ REIT Indices : REIT가 거래되는 것을 기반으로 만든 index (경기가 부동산에 영향을 미쳐서 REIT Index와 Equity는 높은 상관계수를 가진다, Bond와는 낮은 상관계수) * 부동산 편입시 P/F의 Risk감소는 가능하나 Index 구성방식을 고려할 때, 실제 분산효과는 더 낮을 수 있다. * 부동산은 경기, 시장, 이자율 등에 따라 다양하게 영향을 받아 종합적인 판단이 필요 (Regulation에도 크게 영향을 많이 받는다. 구역이나 제도설정 등)

문) Which of the following relates to a benefit when owning real estate directly? A. Taxes B. Capital requirements C. Portfolio concentration

답) A - B, C는 장점이 아닌 단점 (큰규모의 자본필요, 포트폴리오 집중되는 것은 모두 단점) - A (재산세등 단점일 것 같지만, 비용공제 등 세금적인 이익 있음 => When owning real estate directly, there is a benefit related to taxes. The owner can use property non-cash depreciation expenses to reduce texable income and lower the current income tax bill. In fact, accelerated depriciation and interest expense can reduce taxable income below zero in the early years of asset ownership, and losses can be carried forward to offset future income. Thus, a property investment can be cash-flow positive while generating accounting losses and deferring tax payments. If the tax losses do not reverse during the life of asset, depreciation-recapture taxes can be triggered when the property is sold)

Los 60.d) Infrastructure

- Infra투자 : 사회에 Service를 제공하는 시설에 투자 > Brownfield: 기 운영 중인 자산에 대한 투자 (안정적이나 Potential은 좋지 않다) > Greenfield : 신규 운영예정인 자산에 대한 투자 (불안정적이나 Upside potential 존재) - Infra를 건설해서 자체에 운영 or 정부에게 리스를 줄 수도 있다. - Infra는 투자기간이 길고, 비용이 많이 소모, 직접투자는 유동성이 적어 대안으로 ETF나 PE등 고려 - Infra는 분산효과가 있지만 규제, 재무, 현금흐름, 건설, 운영 Risk등을 고려해야 함.

Los 60.e) Commodity

- 원자재 직접투자는 보관비용이 발생 → 주로 파생상품 이용 (Futures, Forwards, Options, Swap 등)

ETF : Commodity or Index에 투자하는 펀드

원자재 생산기업에 투자 : 원자재 가격과 주식가격이 일치하지 않을 수 있음.

Managed Futures Funds : 특정 섹터에 집중하여 선물로 돈을 버는 Fund (헤지펀드처럼 LP형태나 Mutual Funds처럼 주당 거래 가능)

Specialized funds : 특정 원자재에 투자하는 fund

- 역사적으로 Commodity는 주식, 채권보다 수익률, Sharp ratio(리스크당 초과수익률) 낮음, 변동성은 높음 그러나 주식, 채권과의 상관계수가 낮아 P/F편입 시 분산효과 가능 + Inflation Hedge기능 - Future price = Spot price*(1+Rf) + Storage costs - Convenience yield (*contango or backwardation영향) ⓐ Contango : Future > Spot (forwad curve는 upward & roll yield는 negative) ⓑ Backwardation : Future < Spot (cy가 클 때 & forwad curve는 downward & roll yield는 positive)

Contango vs backwardation

- Roll Yield : 선물가격의 변화에서 오는 Return (만기로 갈 수록 Spot Price에 가까워 진다) → Backwardation에서는 Positive, Contango에서는 negative (위 그래프에서 기울기 생각) - Collateral Yield : 실물을 빌려줄 때 발생하는 이자수익 - Change in Spot price : 현물가격의 변화에서 오는 Return

- Timber land : 목재수입, 목재가격에 가치 변동

- Farm land : 곡물수입, 곡물가격에 가치 변동

Los 60.f) Hedge fund

- Hedge fund는 주로 less regulated than TI (투자자가 적어서) + More flexible (Leverage/Long short전략, 파생상품 활용 등) + less liquid (Lockup period / Notice period등 -> 돈 미리 빼려면 Redemptions fee발생) - Prime broker 주로 이용 (Investment를 보관, 관리, 대여, 거래 해주는 직업) - Limited Partner 형태로 조직, Hedge fund firm은 General Partner (<- 관리보수, 성공보수 수령)

구분

설립형태

운용보수 기준

성과보수

Private equity fund

Partnerships

commited capital

보통 투자자들이 최초 투자금액 다 받고나서 수령

Hedge fund

Partnerships

assets under management(NAV)

투자자들이 최초 투자금 받기 전에 수령 *claw back조항

<헤지펀드전략> ① Event Driven : 회사의 변화 Event를 노리고 이익을 취하는 전략 (long-short position strategy) - Merger arbitrage : 사는 회사는 Short, Target회사는 Long - Distressed / Restructuring : 구조조정인 회사의 주식 매수 후 회복한 후 exit - Active shareholder : 경영에 간섭하여 회사 가치 상승시키는 전략 - Special situations : 회사에 특정 이벤트가 발생할 때 투자 (분할, 배당 등)

② Relative value - CB arbitrage : CB 전환가격 vs 보통주 가격 비교 후 매수 - Asset-Back : MBS, ABS 끼리 가격 비교 후 매수 - General Fixed Income : 같은 회사의 채권끼리 가격 비교 - Volatility : 옵션 내재 변동성 vs 매니저가 믿는 변동성 비교 - Multi-Strategy : 다양한 자산들끼리의 비교 후 매수

③ Marco Strategy : Global 거시경제에 베팅(유가, 환율, 나라별 주식시장 등) (long-short position strategy)

④ Equity Hedge Fund (대부분 Bottom-up strategy) - Market neutral : Beta를 0에 가깝게하여 Alpha만 추구 - Fundamental Long/Short Growth : 고성장할 주식 매수, 고평가 주식 short - Fundamental value : 저평가된 주식 매수, 고평가 매도 (short은 잘 안함) - Quantitative directional : 통계기반으로 저평가 매수, 고평가 매도 - Sector Specific : 특정 Sector안에서만 Trading (잘아는 Sector) - Short bias : 주로 Short position 취하는 전략

* Due diligence - 헤지펀드는 소수의 고객 대상, 공시의무나 규제가 약하고 정보 공개의 투명성이 약함 *펀드선택에 있어 어려움 존재 - 숫자화 및 평가하기도 어려움

* Valuation : P/F안의 상장주식은 시장가격, 비상장주식은 Model을 이용하여 추정 (유동성 부족한 주식의 경우 discount적용) (가치평가 시 유동성을 고려하여 평가)

* survivorship(살아남은 firm만 계산에 들어감) & Back-fill bias (index편입 시 좋은 fund만 편입) -> 모두 Return을 upward시키는편향 발생 - Because portfolio companies are revalued infrequently, reported standard deviations of returns and correaltions of returns with equity returns may both be biased downward : "Smoothing effect")'

문) Which of the following statements about commodity investing is invalid? A. Few commodity investors trade actual physical commodities. B. Commodity producers and consumers both hedge and speculate. C. Commodity indexes are based on the price of physical commodities.

답) C Commodity index는 현물상품 가격이 아닌 선물가격을 기준으로 산출된다!

Adverse selection - 역선택 (정보의 불균형으로 인해 불리한 의사결정을 하는 상황)

involvement - 관여, 개입

accredited - 공인된

sophistication - 교양, 개념

side letter (=special term) - 부차적 계약 (특정 조건을 추가하는 계약)

due diligence - 실사, 상당한 주의

committed capital - 약정금액 (투자하기로 약정한 금액)

drypowder - 투자의 목적으로 모금되었으나 실제 투자 집행이 이루어지지 않은 미투자 자금

clawback - 환수

negate - 무효화하다

unitholder - 단위소유자 (unit trust(단위형투자신탁)의 수익자, 펀드의 몇 주 소유한거)

Joint venture - 합작투자

Fund of fund - 재간접 펀드

2 and 20 structure (운용보수 2%, 성과보수 20%의 Fee구조를 의미)

Shortcut methodology(간편법)

dilution : 희석하다

LOS 58.a) AI vs. Traditional <TI(주식, 채권)와 다른 AI>

1. Less liquidity

2. More specialization 3. Less regulation & Less transparency 4. Less available data

5. Different Legal & Tax 6. Fee structure 높음 (수수료 높음) - higher management fees on average and often with additional incentive fees based on performance

7. Derivative 활용도 높음

8. Restrictions on redemptions. (조기상환 어려움) 9. Relatively more concentrated portfolios. * 전통자산인 주식 채권에 대한 leverage, 파생활용하는 전략 역시 AI에 포함됨 유의

-> 포트폴리오 안에 AI 편입 이유 : 분산효과 (TI와 낮은 상관관계) + Higher Return (But 시장에 공포가 커지면 자산들끼리의 상관관계가 증가하므로 효과 없음. *시장떡락 앞에 장사없다 - Although correlations of returns of AI with returns on TI may be lown on average, these correlations may increase significantly during periods of economic stress.)

<Category>

1. Hedge funds : "전략"이 중요 (Leverage전략 / Long Short전략 등) - '전략' + '소수' (이름이 헤지펀드라해서 hedge risk 전략이 필수인 것은 아님 유의)

2. Private equity funds : Invest in the equity of companies to take privage - LBO(차입인수) : established company -> 인수 후 재매각 - Venture capital : early stage -> 초기단기에서 규모가 작은 것을 많이 투자해서 한두개 대박 노림 (Venture capital funds invest in young, unproven companies at various early stages in their lives)

3. Private Debt : Make loans directly to company or invest in debt

4. Real Estate : Invest in residential or commercial properites & Debt & Securities

5. Commodity : Gain exposure to changes in commodity prices (이자, 배당없음 오로지 가격차익으로 이익실현) - Own Physical - Derivatives or Index

- Equity of producing firms

6. Farmland : agricultural land, income form leasing or harvesting

7. Timberland : forest, CF from harvesting

8. Infrastructure: Invest in long lived asstes that provide public services (ex. roads, airports, utility grids, schools, hospitals)

9. Other : Tangible collectible assets (wine or art, etc)

Los 58.b) 투자 방식

1. Direct investing : 자산에 직접 투자 > 장점 : Control, No fee (from fund manager)

> 단점 : 분산효과 낮음, 전문성 필요, higher minimum invsetment amounts ( 발전소를 직접 매입한다고 생각 -> 금액규모도 많이 들어가고, 전문성도 필요하고 분산효과도 낮을 것) 2. Fund investing : Fund를 통해서 여러 자산에 투자 (펀드매니저가 허용된 전략 하에서 투자대상 풀을 선택함, 투자자들은 컨트롤 불가 - the individual investors do not control the selection of assets for investment or their subsequent management and sale.) > 장점 : 분산효과, Expertise 있는 Manager가 운용, lower minimum investment requirements > 단점 : Fee, Manager Risk (*the possibility that the fund manager may perform poorly)

3. Co-investing : Fund에 직접 참여 + Fund 일부분을 자신이 원하는 Asset에 함께 투자 - An investor contributes to a pool of investment funds(as with fund investing) but also has the right to invest directly alongside the fund manager in some of the assets in which the manager invests.) > 장점 : Control, Fee감소 > 단점 : Expertise 필요, 많은 Involve필요, Adverse selection, due diligence(실사) 필요 (Co-investment opportunities may be subject to adverse selection if fund managers choose to make the full investment through the fund for assets they are quite confident about, and offer co-investement opportunities on assets they are less confident about)

Types of AI

Common structure

Infrastructure

Public-private partnership

Real Estate fund investing

Unitholder

Real Estate direct investing

Joint venture

Los 58.c) 투자 & Fee 구조

투자구조 : GP + LP 구조로 Fund 구성 (Limited Partnership) (In a limited partnership, the general partner(GP) is the fund manager and makes investment decisions. The limited partners(LPs) are the investors, who own a partnership share proportional to their investment. The LPs typically have no say in how the fund is managed and no liability beyond thier investment in the partnership. The GP takes on the liabilities of the partnership, including repayment of any partnership debt.) > LP : 투자자, 자기가 투자한 금액만큼만 책임 (Limited Partner) → accredited(공인된) & have sophistication to understand the risks involved) 공인되고 리스크에 대해 이해할 수 있는 투자자가 참여 > GP : Manager, 무한책임사원 (General Partner) → 투자,운영, 분배는 General Partner의 권한

- Limited partnership agreement + speicial terms(LP에게 특별한 혜택을 주는 별도의 Letter : Side Letter)

Fee 구조 : 운용보수(management fee) + 성과보수(incentive fee = performance fee) > 운용보수 : Committed Capital (약정규모)로 결정, Invested Capital (투자한 규모)와 다름! (* Dry powder : 아직미투한 금액) > Committed Capital = Invested Capital + Dry Powder - Fund가 약정규모만큼 조성되면 3~5년에 걸쳐서 투자 집행 ("drawn down(=invested)") - PE는 약정규모의 1~3% 정도로 운용보수를 수령 (*투자한 금액 아니고 약정규모(Commited capital) 기준임 유의) - 성공보수는 Hurdle rate (목표수익률)을 넘어선 이익의 20% 수준 (Fund가 모두 청산되고 나서 성공보수 수령, 그 전에 수령하였으나 막판에 이익이 안좋아지면 -> Claw Back 발동 -> 받았던 성공 보수 반환)

* Hurdle rate : 투자자가 얻고자 하는 목표수익률, 이 수익률을 넘어선 초과이익에 대해서 Incentive지급 ⓐ Soft hurdle rate : Hurdle rate를 넘어서면 전체 이익에 대해서 incentive지급 (a percentage of the total increase) (ex. hurdle rate 8%, 실제 성과 12%인 경우 → 12%*20% = 2.4% 성과보수 지급) ⓑ Hard hurdle rate : Hurdle rate를 넘어선 초과이익분에 대해서만 incentive 지급 (based only on gains above the hurdle rate) (ex. hurdle rate 8%, 실제 성과 12%인 경우 → (12%-8%)*20% = 0.8% 성과보수 지급) ⓒ Catch-up clause : Hurdle rate를 넘어서면, 성과급 배분 비율을 고려하여 gp에게 추가적인 성과 선지급, 그 이후 성과는 다시 원래대로 배분 => Soft hurdle rate과 비슷함 (ex. 성과급 기준 8:2, hurdle rate 10%, Fund 15% 수익인 경우 => 처음 8% 모두 LP몫, 그 이후 2%는 GP몫, 나머지 5%는 8:2로 나누어 가진다)

* High water mark : 이전에 성과보수를 지급했다면, 다음 성과보수는 그때 성과를 넘어서야 지급 가능 (This means that no incentive fee is paid on gains that only offset prior losses. This feature ensures that investors will not be charged incentive fees twice on the same gains in thier portfolio values.) ① American waterfall : Deal by Deal (다른 것이 망해도 잘한 Deal 있으면 성과급 지급) ② European waterfall : Whole of fund (LP가 총 투자원금 회수 후 그 다음부터 성과급 산정, 주로 펀드투자금 모두 끝난 뒤에 지급됨) → LP(Investor)에게는 European 방식이 유리, GP에게는 American 방식이 유리함!

* Clawback provision (환수조항): If the GP accrues or receives incentive payments on gains that are subsequently reversed as the partnership exits deals, the LPs can recover previous incentive payments. (성과보수를 지급했는데, 나중에 결과가 뒤바뀌는 경우 성과보수 환수 가능조항) → A clawback provision would allow the LPs to recover these incentive fees to the extent that the subsequent losses negate prior gains on which incentive fees had been paid.

문1) Alternative investments focus exclusively on the private markets. T/F? 답1) False (주로 사모가 많기는 한데, 헤지펀드, 리츠 등 공모시장에서의 대체투자도 존재)

문2) The distribution method by which profits generated by a fund are allocated between LPs and the GP is called:

A. a waterfall

B. an 80/20 split

C. a fair division

답2) A * 펀드에서 발생한 수익을 배분하는 방식을 "waterfall"이라고 하며 80/20 split은 배분하는 방식 중 하나임

Los59.a) Performance Appraisal

<TI 대비 AI의 추가적인 Risk들>

Lack of transparency

Illiquidity (including restrictions on and performance impact of redemptions)

Complexity

Use of derivatives, securities that are marked to market, leverage

전략의 다양성

Cash drag(PE의 경우 Fund 조성 후 투자까지 시간이 걸림)

=> 추가적인 Risk들을 고려하여 성과 평가 필요함

1. Sharpe Ratio - Sharpe Ratio = [Return - RF] / stadnard deviation (의미 : Risk 한단위당 초과수익률 (excess return per unit of risk)

- 표준편차를 사용하는 것은 적절하지 않음 (Return이 Fat Tail + Negatively skewed이기 때문) - AI는 Real time 거래가 아니라서 표준편차와 상관계수가 실제보다 축소됨(understated) - 상관관계(ρ)를 고려하지 못함.

2. Sortino Ratio - 마이너스 수익률만 고려한 하방표준편차 개념(downside deviation - based on only deviations below the mean return) - 상관관계(ρ)를 고려하지 못함.

* Both the Sharpe and Sortino ratios is that they do not take into account the diversification benefits from low correlations with returns to traditional investments.

3. 그 외 ① Value at Risk : 특정 확률 이내에서의 기대되는 최소 손실 ② Treynor ratio : (Return - RF) / Beta ③ Calmar ratio : Return / Maximum drawdown *보통 연간3년 평균으로 계산함.

4. 성과평가 for Private Capital and Reas Estate ① Money Multiple (Multiple of invested Capital ; MOIC ) (시간가치 고려x)

* Shortcut methodology(간편법) of private equity and real estate

② IRR (시간가치 고려) - 재투자를 가정함 (reinvestment rate가정 + fincancing rate) → Committed Capital을 기반으로 성과평가를 매년 진행할 경우, PE나 부동산 개발 Project는 투자 초기에는 성과가 나쁘다. (오랜 기간에 걸쳐서 투자 과정이 일어나기 때문) → IRR이 성과평가 지표로서 제일 적절함 (IRR over the life of a fund is the most appropriate measuer of after-tax investment performance)

Los59.b) Fee 계산

<문제풀 때 체크해야할 요소들>

Management Fee - Beginning of the year? or End of the year?

Incentive Fee 산정 - Net of management fee? or management fee는 무시?

Hurdle rate - Soft? or Hard?

American / European / High water mark / Claw back?

- Either of fees : 한해에 운용보수 or 성과보수 중 1개만 가져감 = Max[ 운용보수, 성과보수] - Fund 초기에 투자한 투자자는 좋은 조건을 주는 경우가 많다. (founder's shares) - Fund금액을 더 크게 투자하는 경우에 낮은 fee로 협상하는 경우도 있다. (Investors can negotiate for lower fees or better liquidity (shorter lockups and notice periods). Hurdle rates, hard versus soft hurdles, and catch-up provisions may also be subject to negotiation)

Example : Hedge fund fees BJI Funds is a hedge fund with a value of $110 million at initiation. BJI Funds charge a 2% management fee based on assets under management at the beginning of the year and a 20% incentive fee with a 5% soft hurdle rate, and it uses a high-water mark. Incentive fees are caculated on gains net of management fees. (*성과보수는 운용보수금액 차감 후 계산됨) ■ Year 1 : $100.2 million ■ Year 2 : $119.0 million

Caculate the total fees and the investor's after-fee return for both years.

문풀) ■ Year 1 ⓐ management fee : 110 기준으로 계산 (beginning 기준으로 계산하므로) - MF = 110 * 2% = $2.2 million ⓑ Return net of MF : (100.2 - 2.2) / 110 - 1 = - 10.9% ⓒ Incentive fee : 마이너스이므로 성과보수 없음. Total Fees : $2.2 million Year 1 year-end value after fees : $98 million

■ Year 2 ⓐ management fee : ($100.2 - $2.2) * 2% = $98 * 2% = $1.96 million (*전년도 fee차감하고 계산) ⓑ Return net of MF : ($119 - $1.96) / $110 - 1 (*98로 계산 안함, high-water mark) = 6.4% ⓒ Incentive fee : net return $7.04 * 20% = $1.41 million Total Fees : $3.37 million Year 2 year-end value after fees : $115.63million Year 2 after-fee return : 115.63/98 - 1 = 18%

EXAMPLE : Fund-of-funds An investor makes a total investment of $60 million in a fund-of-funds that has a "1 and 10" fee structure, with management and incentive fees caculated independently based on year-end values. $40 million of the investment was allocated to the Alpha fund, and $20 million was allocated to the Beta fund. One year later, the value of the Alpha fund investment is $45 million and the value of the Beta fund investment is $28 million, both net of fund fees. Calculate the investor's return for the year net of fees.

문풀) At year-end, the gross value of fund of funds = $45 + $28 = $73 (million은 생략) ⓐ 재간접펀드의 운용보수 : $73 * 1% = $0.73 ⓑ Return = $73 - $60 = $13 ⓒ 성과보수 = $13 * 10% = $1.3 ⓓ year-end value after fees = $73 - $0.73 - $1.3 = $70.97 ⓔ return rate = 70.97/60 - 1 = 18.3% * 만약에 재간접펀드에 안하고 각각 알파 베타에 투자했으면 73/60-1 = 21.7%의 수익을 올렸을 것.

★EXAMPLE : Waterfall structure and clawback provision A private equity fund invests $100 million in a venture company that is sold for $ 130 million. It also invests $100 million in an LBO that goes poorly and is liquidated for $80 million.

1. If the carried interest incentive fee for the GP is 20% and there is no clawback provision, what is the investor's return after incentive fees, assuming the investment outcomes are realized in the same year: a. under an American style (deal-by-deal) waterfall structure? - 벤처투자 한거 성과보수 따로 (130-100)*20% = $6 지급되고, LBO투자는 지급 X - Return on investment : (130+80-6) / 200 - 1 = 204/200 -1 = 2%

b. under an European style (whole-of-fund) waterfall structure? - 전체 펀드 기준으로 성과 지급 (130+80 - 200) *20% = $2 - Return on investment : (130+80-2) / 200 - 1 = 208/200-1 = 4%

2. How would the answers be affected if the venture investment was sold in year 1 and the LBO investment was sold in year 2? a. American은 어차피 deal by deal이기 때문에 똑같음. b. European인 경우 end-year마다 정산한다면 American과 동일하게 year1에 $6, year2에 fee지급 없음으로 동일하게 된다.

3. How would including a clawback provision effect investor returns caculated in question 1? a. American은 어차피 deal by deal이기 때문에 똑같음 b. European이 year1에 지급한 $6 중 $4는 환수된다.

문1) Advantages of funds-of-hedge funds include due dilligence in selecting individual hedge funds, access to hedge funds that may be closed to direct investments, and dilution of returns to the investor. T/F?

답1) False - The dilution of returns to the investor is a disadvantage for investor. The "due diligence" and "access" attributes are advantages.

LOS 55.a : exercise value, moneyness, time value of an option.

1. 옵션계약 (Options) - 특정자산을 미래의 특정 시점 또는 그 이전에 약정된 가격으로 살 수 있는 권리(Call) 혹은 팔 수 있는 권리(Put)

2. 옵션의 구성항목 ① 기초자산(Underlying asset; S) : 권리행사 시 매수 또는 매도의 대상이 되는 특정자산 ② 만기(Expiration date; T) : 권리를 행사할 수 있는 특정시점 혹은 일정기간의 마지막 날 ③ 행사가격(Exercise price; X) : 권리를 행사할 때 적용되는 가격 ④ 콜옵션(Call option; C) : 살 수 있는 권리, 풋옵션(Put option; P) : 팔 수 있는 권리 ⑤ 옵션프리미엄(Option premium) : 옵션을 매입할 때 지불하는 비용 (권리이기 때문에 옵션을 매입할 때에는 비용이 발생) ⑥ 포지션(Position) : 투자자의 현재상태 - 매입포지션(Long position) : 프리미엄을 지불하고, 옵션을 매입한 사람 - 매도포지션(Short position) : 프리미엄을 받고, 옵션을 매도한 사람.

3. 옵션 vs. 선도계약의 비교

구분

Option Contracts

Forward Contracts

계약의 성격

- Long : 권리만 보유 - Short : 의무만 보유

- Long : 이행의무를 가짐 - Short : 이행의무를 가짐

초기비용

- 초기비용(initial cost)이 0이 아님(they do not have zero value at initiaion) Option premium이 들어감 (권리취득에 대한 비용)

- 초기비용(inital cost)=0

4. 풋옵션 vs 콜옵션

구분

롱포지션(Long)

숏포지션(Short)

콜옵션(call option)

- 기초자산을 살 수 있는 권리 보유 - 옵션의 행사여부를 선택할 수 있음 - 옵션 프리미엄 지불 * 기초자산 Long포지션(가격이 올라야 좋음) ▶ Payoff = Max[0, S-X] ▶ P/L = Max[0, S-X] - Premium ▶ BEP = X+Premium

- 옵션이 행사되는 경우, 기초자산을 팔아야할 의무가 있음. - 옵션 프리미엄 수령 * 기초자산 Short포지션(가격이 내려야 좋음) ▶ Payoff = - Max[0, S-X] ▶ P/L = - Max[0, S-X] + Premium ▶ BEP = X+Premium * Unlimited loss 가능

풋옵션(put option)

- 기초자산을 팔 수 있는 권리 보유 - 옵션의 행사여부를 선택할 수 있음 - 옵션 프리미엄 지불 * 기초자산 Short포지션(가격이 내려야 좋음) ▶ Payoff = Max[0, X-S] ▶ P/L =Max[0, X-S] - Premium ▶ BEP = X- Premium

- PUT 이랑 CALL이 손익이 zero sum이 아니라, 롱/숏 포지션이 zero sum (long call과 shor call의 손익이 zero sum) => Long position과 Short position의 페이오프(payoff)는 정확히 반대! => 콜옵션과 풋옵션의 페이오프는 정반대가 아님 주의!

- A put option gives the buyer the right (but not the obligation) to sell underlying assets at a specified price (=the excercise price = strike price) & The put seller (=writer of the option) takes on the obligation to purchase the underlying assets at the price specified in the option, if the put buyer excercises the option.

- A call option gives the buyer the right (but not the obligation) to buy underlying assets at a specified price(the exercise price) & The call seller (writer) takes on the obligation to sell the underlying assets at the exercise price, if the call buyer exercises the option. - Payoff : 옵션프리미엄(초기비용)을 고려하지 않은 개념. ** 옵션프리미엄은 t=0시점에서 발생한 매몰비용(sunken cost)로, t=T시점에서의 옵션의 행사여부에 영향을 주지 않음! (이미 돈을 만원 주고 복권을 샀다고 하자, 5천원이 당첨됐는데 당청금 수령을 안한다?이미 준 만원으로 손익은 -5천원이어도 무조건 당청금은 일단 수령해야지(매몰비용은 행사여부에 영향x)!) - P/L(손익; Profit/Loss) = Payoff ± 옵션프리미엄

옵션의 Payoff옵션의 profit & loss

* The breakeven point(BEP) for the buyer and seller is the excercise price plus the premium.(X+P) (call) ** The breakeven point(BEP) for the buyer and seller is the excercise price minus the premium.(X-P) (put)

5. 행사방법에 따른 분류 ① 유러피안 옵션 (European options) : 옵션의 만기(At expriation)에 한 번만 행사 가능 ② 아메리칸 옵션 (Americal options) : 옵션의 만기일을 포함하여 언제든지(at anytime) 행사 가능 -> 한번 행사 하면, 옵션은 소멸

* 아메리칸 옵션 보유자의 선택권

유러피언 옵션 : 옵션을 만기에도 행사할 수 있음

조기행사 옵션 (Early excercise option) : 만기 이전에도 옵션을 행사할 수 있음.

아메리칸 옵션 보유자는 2가지 옵션을 모두 보유하고 있으므로, 2개의 옵션 중 큰 값이 아메리칸 옵션의 가치임. Americal option = Max [①European option, ②Early exercise option] ** American option value ≥ European option value

American option = MAX [①European option, ②Early exercise option]

아메리칸 콜옵션(C_t,A) : 유러피언 콜옵션과 Lower bound가 동일 ▶ C_t,E ≥ MAX[0, St - X/e^R(T-t)] & 조기상환옵션 = MAX[0, St-X] ▶ St- X/e^R(T-t) > St-X 이므로 C_t,A ≥ MAX[0, St - X/e^R (T-t) ] (유러피언 콜옵션과 동일)

아메리칸 풋옵션(P_t,A) : 유러피언 풋옵션과 동일하지 x ▶ P_t,E ≥ MAX[0, X/e^R(T-t)-St] & 조기상환옵션 = MAX[0, X-St] ▶ X/e^R(T-t) - St < X - St 이므로 P_t,A ≥ MAX[0, X-St] (유러피언 풋옵션과 동일X)

Option

Minimum Value

Maximum value

European Call

C_t,E ≥ MAX[0, St-X/e^R(T-t)]

St

American Call

C_t,A ≥ MAX[0, St-X/e^R(T-t)]

St

European Put

P_t,E ≥ MAX[0, X/e^R(T-t)- St]

X/e^R(T-t)

American Put

P_t,A≥MAX[0, X - St]

X

12. 이항모형 (Binomial Tree Model)

Option Valuation Model or Option Pricing Model (OPM) ① Black-Sholes Formula ② Binomial Tree Model (CFA lv1 : One-Period Binomial Tree Model) ③ Monte-Carlo Simulation

Binimial Tree Model - 기초자산의 수익률이 이항분포를 따른다고 가정 : 1기간 후의 주가는 일정한 비율로 상승하거나 일정한 비율로 하락

S0 = $50, Su = $60, Sd = $42, u = 1.2, d=0.84, X = $55, Rf = 3%

=> 헷지포트폴리오 : Vu = Vd -> -5 + 60h = 42h -> h= 0.278 일때 Vu=Vd=$11.68 V0 = -C0+hS0 이므로 대입하면 C0의 가격을 구할 수 있다. -> V0 = 11.68/(1.03) = -C0+0.278*50 -> C0 = $2.56

** h : Hedge Ratio ( = Option's Delta) : Call option은 기초자산인 주가가 움직일 때, Delta만큼 가격이 변동하는 민감도를 가지고 있다. 따라서 기초자산을 h개만큼 보유하고 있으면 Short call의 손익과 주식의 손익이 상쇄되어 무위험 포트폴리오 구축이 가능하다.

이항모형 with risk-neutral probability of an up-move or a down-move U : 주가상승률 D : 주가하락률 = 1/U πu : 위험 중립가정 하의 상승확률 πd : 위험 중립가정 하의 하락확률 (= 1 - πu) * 이 확률은 실제 확률이 아님 (These two probabilities are not the actual probabilities of the up and down moves. They are risk-neutral pseudo probabilities.)

One-period binomial model for valuing an option : 확률 필요없음. (상승, 확률일때의 Payoff정보만 필요)

One-period binomial model based on risk neutrality (no-arbitrage relationship을 쓰기 때문에 위험중립확률이 필요) - the value of an option = a probability-weighted average of two possible outcomes. - 옵션가격에 미치는 것은 Rf (Risk free rate)과 Volatility (Ru - Rd = difference between the up and down gross returns) - 변동성이 커질수록 옵션가격은 올라간다 (콜, 풋 모두)

* 문) When using a one-period binomial model to price a call option, an increase in the actual probability of an upward move in the underlying asset will result in the call option price?

답) 실제 확률은 Call option price에 아무런 영향을 미치지 않는다! (staying the same)

Interest rate futures (금리선물) - 선물시장 내 금리 혹은 채권을 기초자산으로 하는 선물계약을 의미

Basis Point Value (BPV) : 시장금리(MRR)가 1bp 움직일 때, 금리선물 1계약의 가치변동분을 의미

zero rate = spot rate (현물금리)

par swap rate = 스왑계약의 고정금리

LOS 53.a : 선도계약과 선물계약의 가치평가 비교

* 선도계약과 선물계약의 가장큰 차이는 Margin call

1. 선물계약 (Futures Contracts)

미래의 특정 시점에 특정 기초자산을 미리 정한 가격으로 매매하기로 약정하는 계약 (선도계약의 정의와 동일)

거래조건(기초자산, 만기일 등)을 규격화 한 후 거래소에 상장시켜 거래하는 형태의 선도계약을 선물계약이라고 한다.

구분

선도계약

선물계약

공통점

정산방법(Settlement) : Physical Delivery(실물인수도), Cash Settlement(차액정산) 모두 가능

계약시점의 파생상품 가치 = 0 (V0(T) = 0) (가치는 0인건 똑같은데, 선물은 증거금으로 초반에 돈(개시증거금, initial margin)이 들어감, 비용으로 보는 것이 아님!)

차이점

- 거래조건

거래방법, 계약단위, 만기일 등 제한 없음

거래방법, 계약단위, 만기일 표준화

- 거래장소

당사자 간에 직접거래 (장외거래 OTC)

규정된 거래소에서 거래(exchange trade)

- 이행보증

거래당사자 간의 신용 * 최근 CCP가 도입됨.

청산소(CCH ; Clearing House)에서 이행보증

- 증거금

규정된 증거금 없음

증거금제도 있음

- 정산방법

일반적으로 선도계약 종료일에 정산

일일정산

- 신용위험

거래상대방위험(counterparty risk) 존재

거래상대방위험 없음. (물론 아예 없는 것 아니지만 CFA교재상대로 없는 것으로)

선물계약의 주요 특성 ① 거래소 (Exchange) : 선물거래시장은 정형화되고, 조직화되고 규격화된 시장 (KRX, CBOT, CBOE) ② 청산소(Clearing House) *한국은 거래소와 청산소가 같은데, 두개가 다른 곳인 나라도 있음. - 모든 선물거래 상대방이 됨으로써 선물 거래의 이행을 보증하고, 선물거래의 손익을 정산해주는 기관 - 선물거래는 청산소의 이행보증 덕에 거래상대방위험(Counterparty risk)이 없음. ③ Novation : 사적계약을 거래소와의 계약으로 갱신함.

정산가격(Settlement price) = ST (선물계약의 만기일에 선물계약을 정산할 때 사용하는 현물가격, 만기일 종가) ▷ (Long Position) Payoff = ST- FP ▷ (Short Position) Payoff = - (ST- FP) * FP = S0*(1+Rf)^(T)로 선도계약과 Pricing 식은 동일함.

Offsetting or Reverse Trade - 선물계약은 만기에 정산하지 않고, Offsetting trade(청산매매, 반대매매)를 통하여 거래를 청산할 수 있음. - Offsetting Trade : 만기 이전에 처음 선물 거래와 반대 포지션의 거래를 통하여 최초 선물 거래를 청산하는 것.

선물시장 참여자 - Hedgers : 현물가격의 가격 변동위험을 관리하기 위해 선물시장에 참여하는 사람 (헤지목적) - Speculators : 현물을 보유하지 않은 상태에서 산물시장에만 참여하는 사람 (선물가격의 방향성에 Betting)

일일정산 (Daily Settlement), Marking to Market (MTM) - 일일정산 : 선물가격 변화에 의한 손익을 매일매일 정산하여 증거금 계좌 (Margin account)에 반영 - Daily Settlement와 MTM을 혼용하여 사용.

증거금제도(Margin Account) => 레버리지를 가능하게 한다! - Performance guarantee(계약이행보증금) : 선물계약 당사자가 계약을 이행하지 않을 수 있는 위험을 대비하기 위해 거래소가 징수하는 계약이행보증금 - Initial Margin(개시증거금) : 선물거래를 시작하기 위해 납부해야하는 증거금 - Maintenance Margin (유지증거금) : 거래를 지속하기 위해 반드시 유지해야하는 증거금 - Variation Margin (변동증거금, 추가증거금) : 거래자의 증거금이 유지증거금 이하로 감소하였을 경우, 증거금을 *개시증거금 수준으로 올리도록 추가적인 증거금의 적립을 요구함 (Margin call)

* 유지증거금 수준이 아니라 개시증거금수준으로 올려야 하는 것에 유의 (주식계좌는 유지증거금까지, 파생은 개시증거금까지 채워넣어야 함)

Price Limits (1일 가격 변동한도) - 거래소에서 부과하는 선물계약의 일일변동 폭 - Limit Up : 일일변동할 수 있는 상한 가격 - Limit Down : 일일변동 할 수 있는 하한가격 - Limit Move : 상한 가격과 하한가격 사이의 제한된 움직임

CCP (Central Counterparty) - OTC거래에서 거래상대방 간 정산업무를 수행할 수 있도록 지정한 기관(선물의 청산소, 거래소와 유사한 역할) - OTC거래에서의 Counterparty risk를 통제하기 위해, 담보(Collateral)를 관리하는 것이 일반적.

금리선물(Interest rate Futures) - 기초자산을 금리(이자율) 또는 채권으로 하는 선물 계약 (MRR or T-bonds) *채권도 금리선물이라고 칭함) - 금리선물의 표준화된 거래형태 ⓐ 결제방식 : 현금정산 (Cash Settlement) ⓑ ★ 가격공시 방식 ★ (그냥 외우기)

===> Futures price = 100 - Annualized MRR in percent - (ex) 6개월 후 6개월 짜리 금리를 기초자산으로 하는 Futures price = 97, F(6m, 6m) = MRR(6m, 6m) = 3%에 거래한다는 것.

Basis Point Value (BPV) : 시장금리(MRR)가 1bp 움직일 때, 금리선물 1계약의 가치변동분을 의미 - BPV = notional principal * period * 0.01% - one basis point change in the MRR will change the future contract value by BPV.

* 반면에 선도계약의 가치변동은 Convex하다 (금리오르면 변동폭 감소, 하락하면 변동폭 증가) > 1bp상승 시 FRA payoff = (0.01%)*$1milion*(6/12)/(1+2.51%/2) = 50/(1+2.51%/2) = $49.3803 > 1bp하락 시 FRA payoff = (-0.01%)*$1milion*(6/12)/(1+2.49%/2) = 50(1+2.49%/2) = -$49.3852 Convexity bias of Interest rate futres and forward==> 위와 같이 선물과 선도가치가 기간이자율이 길어질 수록 커지는 것을 Convexity Bias라고 한다. (The convexity of forwards is termed convexity bias and forwards and futures prices can be significantly different for longer-term interest rates.) * MRR이 떨어지는 경우가 올라갈때보다 가격차이의 정도가 큼

선물 및 선도계약의 비교 - 일일정산에 따른 차이 - 일일정산 후 선물가격은 종가로 변경됨. - 선물은 일일정산 후 Initial Margin에 대한 초과금액은 인출하고 재투자할 수 있음.

- A positive correlation between interest rates and the futures price means that (for a long position) daily settlement provide funds (excess margin) when rates are high and they can earn more interest, and requires funds (margin deposits) when rates are low and opportuinity cost of deposited funds is less. (Futures가 이론적으로 더 매력적) > 정리 < ⓐ Corr(이자율, 선물가격) = 0 → Futures나 Forward나 무차별 (동일) ⓑ Corr(이자율, 선물가격) > 0 → 선물가격 오르면 예치금이나 재투자 이자 더 받고, 내리면 자금 조달비용이 적게드므로 Futures > Forward (선물 선호) ⓒ Corr(이자율, 선물가격) < 0 → 선물가격 오른 경우 더 낮은금리이자, 하락하면 조달금리 비용 상승으로 Futures < Forward (선도 선호)

LOS 54.a : 스왑계약의 가격결정, 가치평가

Forward Contracts Pricing : 선도가격을 결정하는 프로세스 - V0(T) = 0이 되도록 하는 F0(T) <- No arbitrage Forward Price

Swap Contracts Pricing : 스왑계약의 고정금리(Swap-fixed rate)을 결정하는 프로세스 - V0(T)=0이 되도록 하는 Swap Fixed Rate의 결정 (똑같이 No-arbitrage Pricing) - 변동금리의 현재가치와 고정금리의 현재가치가 동일하도록 고정금리를 산정함 = Par Swap Rate(F) - Spot Curve와 동일한 하나의 금리(Par Swap rate)을 산출하는 것이 Swap Contracts Pricing이다! ∑PV(Pay amount) = ∑PV(Recive amount) * FRA로 Replication할 수 있는데, 다만 스왑의 V0(T)=0을 만들기 위한 각각의 복제된 FRA 가치는 0이 되지 않을 수 있다. (합쳐야 0이됨)

F = Par Swap Rate = fixed rate payment = the price of a fixed-for-floating interest-rate swap *최초에 정해짐

MRR = forward day rates implied by the spot rates S = current effect spot rates for each period. (zero rate라고도 한다)

** The price of a fixed-for-floating interest-rate swap is specified in the swap contract. ** 고정금리 수취 포지션을 취할 시 이는 채권 long position과 같으므로 포트폴리오의 duration 상승 가능.